Financial developments in 2025

Despite periods of significant financial turmoil, the global economy performed robustly in 2025, contributing to healthy returns, particularly in the equity markets.

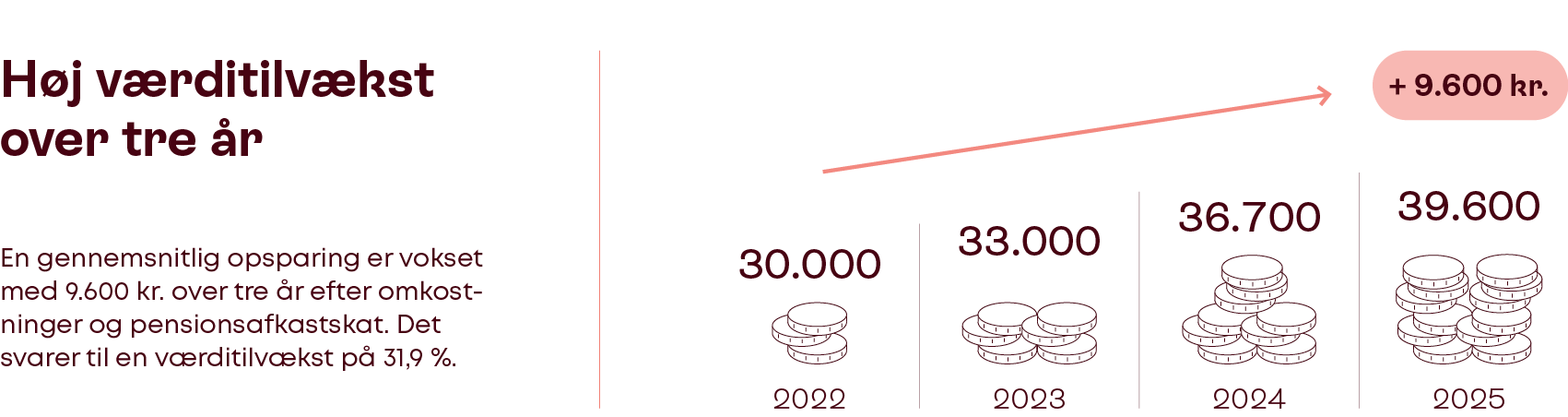

2025 turned out to be a good year for investment, with positive returns on shares, bonds and credit investments. At the start of the year, the launch of the Chinese AI model, DeepSeek, triggered a fall in the prices of US technology shares. The turmoil became more widespread and culminated following the announcement of substantial US tariff increases on 2 April. However, the equity market recovered towards the summer, partly as a result of postponements and downward revisions to the tariff rates.

Global economic growth exceeded expectations in 2025 despite the financial turmoil. In the US, significant investment in artificial intelligence (AI) infrastructure underpinned growth. At the same time, both European and US companies demonstrated a high degree of adaptability to the new trading conditions, which was reflected in strong financial results. This contributed to the stock markets delivering high returns.

In the US, the rise in share prices was broad-based, but continued to be led by some of the largest US technology companies. In Europe, improved growth prospects and extensive fiscal policy initiatives contributed to the sharp rises in share prices. In Denmark, sharp falls in share prices, including those of Novo Nordisk, led to a more subdued performance.

The year was also characterised by global monetary policy easing. However, the prospect of significantly higher bond issuance in Europe caused European bond yields to rise. This led to capital losses on high-grade bonds, which consequently generated a lower return than in the previous two years. The strong economy led to a strong year for credit investments as a result of narrowing credit spreads.

The US dollar fell sharply in 2025, primarily due to increased uncertainty surrounding trade policy and concerns about the direction of US fiscal policy. This had a negative impact on many Danish investment funds, but the investments held by LD Pensions were well protected by a high level of hedging against currency exposure to the US dollar, which boosted members’ returns.